Specialty chemicals are highly tailored materials engineered for precise applications, distinguishing them from mass-produced commodity chemicals. These materials are critical in industries like pharmaceuticals, electronics, and personal care, where they enhance product quality and meet strict regulatory standards. For example, they play a key role in electric vehicle (EV) batteries and semiconductor manufacturing, with specialty chemicals accounting for 9–14% of electronic device components.

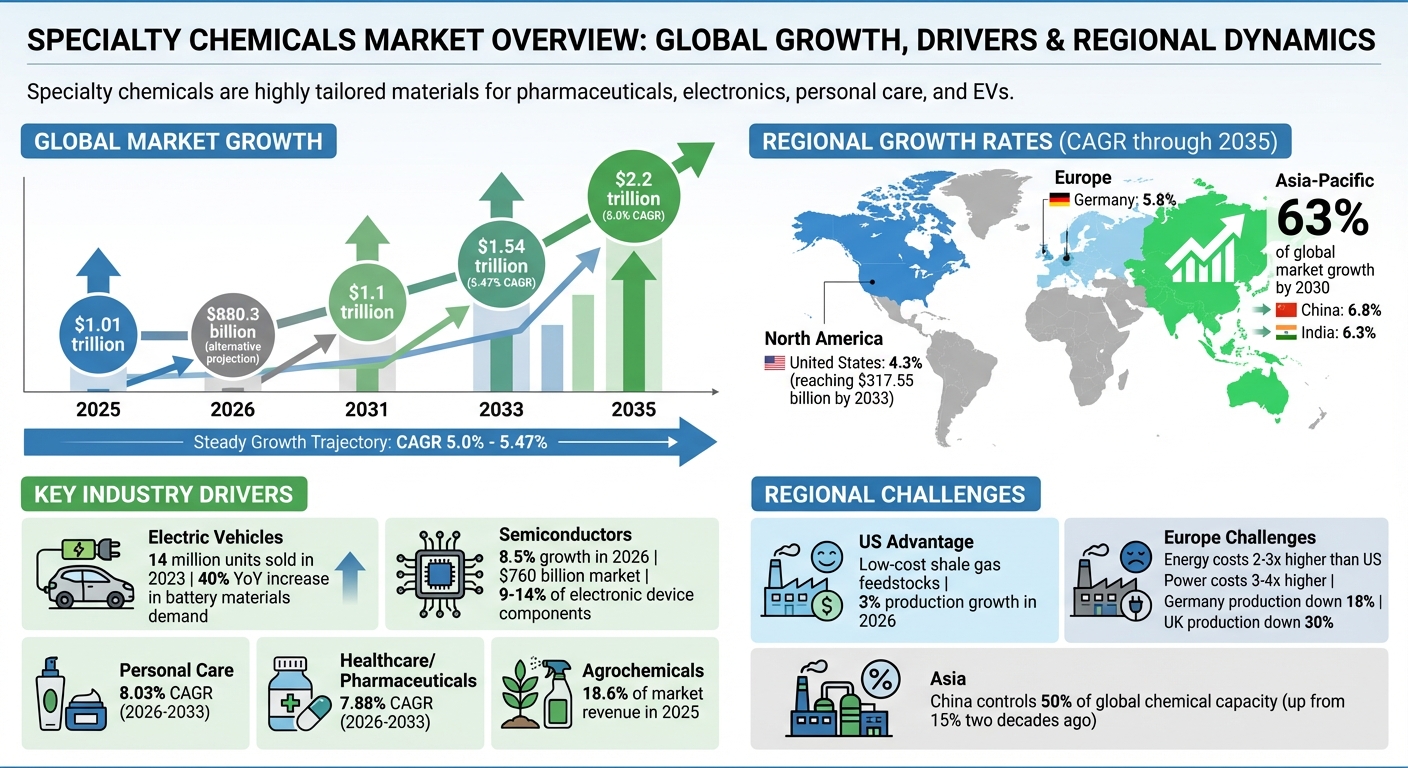

The global specialty chemicals market is projected to grow from $880.3 billion in 2026 to over $1.1 trillion by 2031, driven by sectors such as AI data centers, 5G infrastructure, and battery technologies. The Asia-Pacific region leads this growth, contributing 63% of market expansion by 2030, with China and India showing strong demand. Meanwhile, the U.S. benefits from low-cost shale gas feedstocks, bolstering its competitiveness, while Europe faces challenges like high energy costs and stricter regulations.

Key trends include:

- Electric Vehicles: EV sales surged to 14 million units in 2023, driving demand for advanced battery materials.

- Semiconductors: Expected 8.5% growth in 2026, increasing the need for ultra-pure chemicals.

- Personal Care and Pharmaceuticals: Rapid growth, with personal care chemicals projected to grow at 8.03% CAGR from 2026 to 2033.

Challenges such as fluctuating feedstock costs, supply chain disruptions, and geopolitical tensions are reshaping global production strategies. Producers are shifting focus to higher-margin specialty products to offset rising costs, with price hikes seen across materials like phenol, styrene, and titanium dioxide in early 2026.

Sustainability is also a growing priority, with companies investing in low-carbon production and bio-based solutions. For instance, BASF and Evonik are advancing green chemistry practices to meet evolving market demands. In this dynamic landscape, sourcing strategies and strong supplier relationships are critical for ensuring reliability and compliance.

Global Specialty Chemicals Market Growth 2025-2035: Regional Trends and Key Industry Drivers

Rising Global Demand for Specialty Chemicals

Market Size and Projected Growth Rates

The specialty chemicals market is on a growth trajectory, driven by advances in technology and expanding applications. Estimates place the global market’s value at approximately $1.01 trillion in 2025, with projections suggesting it could climb to $1.54 trillion by 2033, reflecting a compound annual growth rate (CAGR) of 5.47% [5]. Some analysts forecast even higher growth, predicting the market might reach $2.2 trillion by 2035, with a slightly lower 5.0% CAGR [6]. These differences arise from varying methodologies and definitions of the sector.

The Asia-Pacific region is set to dominate, contributing an estimated 63% of the global market’s incremental growth between 2025 and 2030 [7]. Within this region, China is expected to lead with a robust CAGR of 6.8% through 2035, followed by India at 6.3% and Germany at 5.8%. Meanwhile, the United States is projected to grow at a more modest 4.3% CAGR during the same period [6], with its market value anticipated to reach $317.55 billion by 2033 [5]. Key growth areas in the U.S. include semiconductor manufacturing and pharmaceutical production, which are fueling demand for high-performance specialty chemicals.

These varied growth rates highlight the importance of industry-specific drivers in shaping the market’s future.

Industries Driving Demand Growth

Electric vehicles (EVs) and battery technologies are among the most influential factors driving demand for specialty chemicals. In 2023, global EV sales surpassed 14 million units, spurring a 40% year-on-year increase in demand for battery materials [8]. This boom has created a need for specialized products like advanced electrolytes, thermal management fluids, and cathode materials that meet stringent performance requirements. For example, in January 2025, BASF SE partnered with leading battery manufacturers to develop next-generation electrolyte formulations for solid-state batteries, aiming for commercial availability by 2027 [2].

The electronics and semiconductor industries are also pivotal. Demand for ultra-high-purity chemicals and specialty gases continues to rise as these sectors expand. India’s semiconductor market, for instance, is projected to grow from $24 billion in 2022 to $110 billion by 2030, significantly boosting demand for electronic-grade specialty chemicals [8]. In the U.S., semiconductor fabrication is expected to account for 18% of the specialty chemicals market by 2036 [1]. The push for 5G infrastructure, AI-driven data centers, and miniaturized technologies further fuels the need for materials like photoresists, wet chemicals, and thermal interface compounds with exacting purity standards.

Pharmaceuticals and personal care are also seeing rapid growth, spurred by changing consumer habits and evolving regulations. The personal care segment is forecast to achieve the fastest growth, with a CAGR of 8.03% from 2026 to 2033, while healthcare applications are expected to grow at a 7.88% CAGR during the same period [5]. Reflecting this trend, BASF launched "Verdessence Maize" in April 2025, a plant-based specialty chemical designed for the personal care and cosmetics industry [5]. Additionally, the agrochemical sector is projected to account for 18.6% of market revenue in 2025, driven by global food security challenges and the demand for high-efficiency crop protection solutions [6].

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

sbb-itb-aa4586a

Regional Production Patterns and Output Differences

US Production Benefits from Shale Gas

The United States holds a leading position in specialty chemical production, thanks to its access to low-cost shale gas. Ethane feedstocks derived from shale formations give US producers a major cost advantage over regions reliant on naphtha, which is more vulnerable to fluctuations in global oil prices. According to the American Chemistry Council, US chemical production is expected to grow by about 3% in 2026, reflecting the country’s strong energy resources [11].

This cost edge has helped shield US producers from the plant closures and industry downsizing seen in other regions. Martha Gilchrist Moore, Chief Economist at the American Chemistry Council, highlighted this resilience:

"With gains in ethane production driven by increased natural gas output, our competitiveness remains very, very positive for US chemical manufacturing" [10].

Major investments continue to flow into the US chemical sector. One notable example is the $8.5 billion Golden Triangle Polymers project in Texas, a joint venture between Chevron Phillips Chemical and QatarEnergy, set for completion in 2026 [10]. Additionally, in July 2025, Air Liquide announced significant greenfield investments in ultra-pure gases and solvents to support the growing US semiconductor industry and the reshoring of chip manufacturing [3]. Meanwhile, higher energy costs and overcapacity create challenges for producers in other regions, leading to contrasting industry dynamics.

Europe and Asia Face Different Challenges

While the US enjoys a feedstock cost advantage, regions like Europe and Asia grapple with unique economic and production hurdles. These disparities play a key role in shaping the global specialty chemicals market.

In Europe, chemical producers face a structural downturn rather than a temporary slowdown. Energy costs in the region are 2–3 times higher than in the United States, with power costs reaching 3–4 times US levels, leaving European manufacturers at a competitive disadvantage [9][11]. Between 2019 and Q2 2025, Germany’s chemical production fell by 18%, while the UK experienced a 30% decline, underscoring the challenges [11]. Analysts from Oliver Wyman explained:

"For the European chemicals industry, the current downturn is structural, not cyclical. Besides stubbornly high energy prices, the sector also faces more stringent regulation than producers in other regions" [11].

Asia presents a more varied landscape, shaped by overcapacity and regional differences. China, now responsible for about 50% of global chemical capacity, has significantly increased its market share from 15% two decades ago [11]. This rapid expansion has driven global operating rates down to around 70% in many European countries, well below historical norms [9]. To adapt, producers in Japan and South Korea are restructuring. Japan plans to retire three naphtha crackers by 2028, while South Korea is targeting reductions of 2.7–3.7 million tons per year [9]. Both nations are shifting toward higher-margin specialty chemicals to reduce their reliance on volatile commodity markets and maintain profitability in a competitive global environment.

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

Supply Chain Factors and Feedstock Availability

Lower Feedstock Costs Benefit Producers

The cost of raw materials plays a critical role in determining profitability in the specialty chemicals industry. For example, fluctuations in crude oil prices directly impact petrochemical costs, often squeezing profit margins [4]. In contrast, producers in the United States benefit from an ample supply of ethane, which lowers feedstock expenses compared to regions reliant on naphtha [3].

This cost disparity is reshaping global production strategies. European facilities, for instance, are being retrofitted to process US ethane instead of naphtha, helping offset the burden of high energy prices [3].

Supply Disruptions and Capacity Adjustments

Geopolitical issues and shifting trade policies are testing the resilience of supply chains. For example, tensions in the Red Sea have extended Gulf-to-Asia shipping routes by 8–12 days, delaying feedstock deliveries and driving up logistics costs [3]. These challenges have encouraged companies to rethink their inventory strategies, moving away from just-in-time systems toward more robust stockpiling methods.

Uncertainty in trade policies has also disrupted import patterns. In March 2025, US chemical imports reached a high of over $20 billion, only to decline to $17 billion in April 2025 [3]. Imports from China saw a sharp 30% drop in Q2 2025 as companies shifted sourcing to Southeast Asia for materials like resins and basic chemicals [3]. At the same time, agricultural chemical production is expected to increase by 3.6% in 2025 before contracting by 1.3% in 2026 [12].

These shifts in feedstock costs and supply chain disruptions are likely to influence pricing trends as the industry moves into 2026.

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

Pricing Trends and Profit Margins

Producer Price Increases in 2026

Manufacturers are responding to rising production costs by increasing prices. In February 2026, industry-wide producer prices rose by 0.8%, driven not by strong demand but by the need to maintain profit margins in a tough cost environment.

Several key producers announced price hikes in March 2026. Sinopec North China raised phenol prices by 500 yuan per ton on March 3. On March 4, Wanhua Chemical increased styrene prices by 250 yuan per ton, and Luxi Chemical made a similar adjustment for trichloromethane [13]. These changes were largely influenced by a 10% spike in crude oil and methanol futures, which stemmed from geopolitical tensions in the Strait of Hormuz [13][14].

Later, on March 17, 2026, LANXESS announced a 20% price increase for trimethylolpropane (TMP), citing sustained rises in energy costs and higher prices for petrochemical feedstocks like formaldehyde and n-butyraldehyde [17]. Similarly, Tronox Holdings raised titanium dioxide prices by 2% to 4% during Q1 2026 [16].

These price increases highlight a broader trend, as manufacturers pivot toward higher-margin specialty products to strengthen their financial performance.

Shift Toward Higher-Margin Products

In response to cost pressures and market conditions, manufacturers are shifting their focus from high-volume commodity chemicals to specialty products that offer better margins. Commodity chemicals often face price challenges due to global overcapacity, while specialty products can command premium prices and avoid commoditization [15][16].

The semiconductor industry showcases this trend effectively. With an expected growth rate of 8.5% in 2026, the sector is projected to exceed $760 billion globally. This growth is fueling demand for ultra-pure gases and solvents, which are essential for chip production and represent lucrative opportunities for specialty chemical suppliers [15]. Specialty chemicals now account for 9%–14% of the materials cost in electronic devices, making this market particularly appealing.

Manufacturers are also leveraging permanent capacity reductions to stabilize pricing. For instance, Tronox shut down its Fuzhou plant in January 2026, following the closure of its 90,000-metric-ton Botlek facility in March 2025. These moves have helped establish a price floor, even amid weak demand in the construction sector [16]. Similarly, The Chemours Company sold the land of its former Kuan Yin site in Taiwan for $360 million, reallocating resources toward higher-margin chloride-process titanium dioxide production [16].

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

Industry Movement Toward Specialty Products

Development of Sustainable Chemical Solutions

Sustainability has become a non-negotiable aspect of modern supply chains, with suppliers now expected to provide documented carbon data, traceability, and compliance evidence [18]. As the demand for chemical building blocks is projected to double by 2080, the industry could require up to $1 trillion in capital to meet these needs [3]. To address this, manufacturers are increasingly adopting green chemistry practices. These include low-carbon production methods, energy-efficient processes, and the use of recyclable, low-VOC solvents. Measures like solvent recovery and heat integration are also gaining traction, aiming to reduce toxicity and emissions [18].

Recent investments highlight this shift. BASF SE has partnered to commercialize next-generation electrolytes by 2027 [2], while Evonik Industries has allocated EUR 100 million to bio-based surfactants for sustainable personal care and cleaning products [2]. According to Royalchem, sustainability is now seen as "a more reliable option", offering benefits like reduced compliance risks, fewer disruptions, and better audit readiness [18]. This growing emphasis on sustainable innovation aligns seamlessly with strategic sourcing practices supported by specialized providers.

Allan Chemical Corporation‘s Sourcing Approach

In this evolving landscape, Allan Chemical Corporation stands out with its sourcing-first strategy, designed to ensure both compliance and reliability. The company supplies chemicals for industries such as pharmaceuticals, food, cosmetics, ceramics, and electronics, focusing on just-in-time delivery, competitive pricing, and strong supplier relationships. This approach ensures consistent product availability, even during market fluctuations.

Allan Chemical Corporation provides both technical-grade and compendial-grade solutions (USP, FCC, ACS, NF), backed by thorough documentation like Certificates of Analysis and Safety Data Sheets. This commitment to detailed documentation aligns with the industry’s increasing need for traceability and compliance-ready supply chains [18]. By maintaining direct relationships with vetted manufacturers, the company offers flexibility in batch sizes, expedited delivery, and custom packaging options tailored to meet specific customer requirements. This approach not only mitigates supply chain risks but also addresses the growing regulatory demands of today’s market.

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

Why Specialty Chemicals Could Be India’s $1 Trillion Story?

Conclusion

The specialty chemicals market is undergoing significant changes, shaped by a mix of economic trends and technological advancements. Global demand is on the rise, fueled by industries like semiconductors and electric vehicles. The Asia-Pacific region is projected to account for 63% of global market growth by 2030, while North America and Europe concentrate on developing high-value products [7]. These trends highlight distinct approaches to production across different regions.

Regional dynamics reveal unique challenges and opportunities. In the U.S., access to low-cost shale gas provides a competitive edge, whereas Europe faces hurdles such as high energy costs and strict regulatory frameworks that impact operational efficiency. Additionally, supply chain disruptions and fluctuations in feedstock prices – potentially affecting producer margins by up to 10% each quarter – emphasize the need for sourcing custom chemical blends [7].

The industry is increasingly focusing on higher-margin products that align with evolving regulatory and market expectations. Investments in sustainable solutions and innovative practices reflect this shift, illustrating how economic and regulatory forces are reshaping the market [3].

In this evolving landscape, experienced companies like Allan Chemical Corporation play a vital role. With over four decades of expertise in regulated industries such as pharmaceuticals, food, cosmetics, ceramics, and electronics, the company offers both technical-grade and compendial-grade solutions (USP, FCC, ACS, NF). Their just-in-time delivery model, competitive pricing, and strong partnerships with manufacturers help customers navigate challenges like market volatility, complex regulations, and supply chain risks —including evolving fragrance safety regulations – ensuring reliable product availability.

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

FAQs

Why is Asia-Pacific driving most specialty chemicals growth?

The Asia-Pacific region is driving growth in the specialty chemicals market, fueled by increasing demand for high-performance materials across sectors like electronics, pharmaceuticals, and automotive. This surge is supported by rapid industrialization, technological progress, and initiatives aimed at sustainability. Leading companies in the region are focusing on high-margin products, such as materials for semiconductors and batteries, to stay competitive. Countries like Japan, China, and India are pivotal in this expansion, solidifying Asia-Pacific’s position as a global leader in the specialty chemicals industry.

How do feedstock and energy costs change where chemicals are made?

Feedstock and energy costs play a major role in determining where chemical production takes place, as they significantly affect manufacturing expenses. When prices for energy or raw materials rise, producers often shift operations to regions where these inputs are more affordable. Areas with plentiful natural resources or lower energy costs tend to attract production facilities. Additionally, unpredictable changes – like geopolitical tensions or supply chain issues – can drive companies to reevaluate and relocate production to control costs and stay competitive in the specialty chemicals industry.

What can buyers do to reduce price and supply risk in 2026–2031?

To reduce price and supply risks in the period from 2026 to 2031, buyers can take proactive steps. One approach is nearshoring, which involves shifting supply chains closer to home. This strategy lessens reliance on international suppliers and helps avoid disruptions tied to trade and logistics. Another effective method is performing total cost of ownership (TCO) analyses. These evaluations reveal hidden expenses often overlooked in global sourcing, giving a clearer picture of overall costs.

In addition, adopting digital supply chain tools can make a big difference. These tools enhance demand forecasting, provide real-time tracking, and improve communication with suppliers. Together, they boost flexibility and strengthen supply chain resilience, making it easier to navigate unpredictable market conditions.

Comments are closed