In 2025 and 2026, U.S. trade policies have significantly impacted niche chemical industries by increasing costs and disrupting supply chains. Tariffs on specialty chemical intermediates, often sourced from China, have left manufacturers with limited alternatives. Key sectors – pharmaceuticals, electronics, and ceramics – are grappling with rising expenses and production delays, creating challenges for both domestic and global operations.

Key Takeaways:

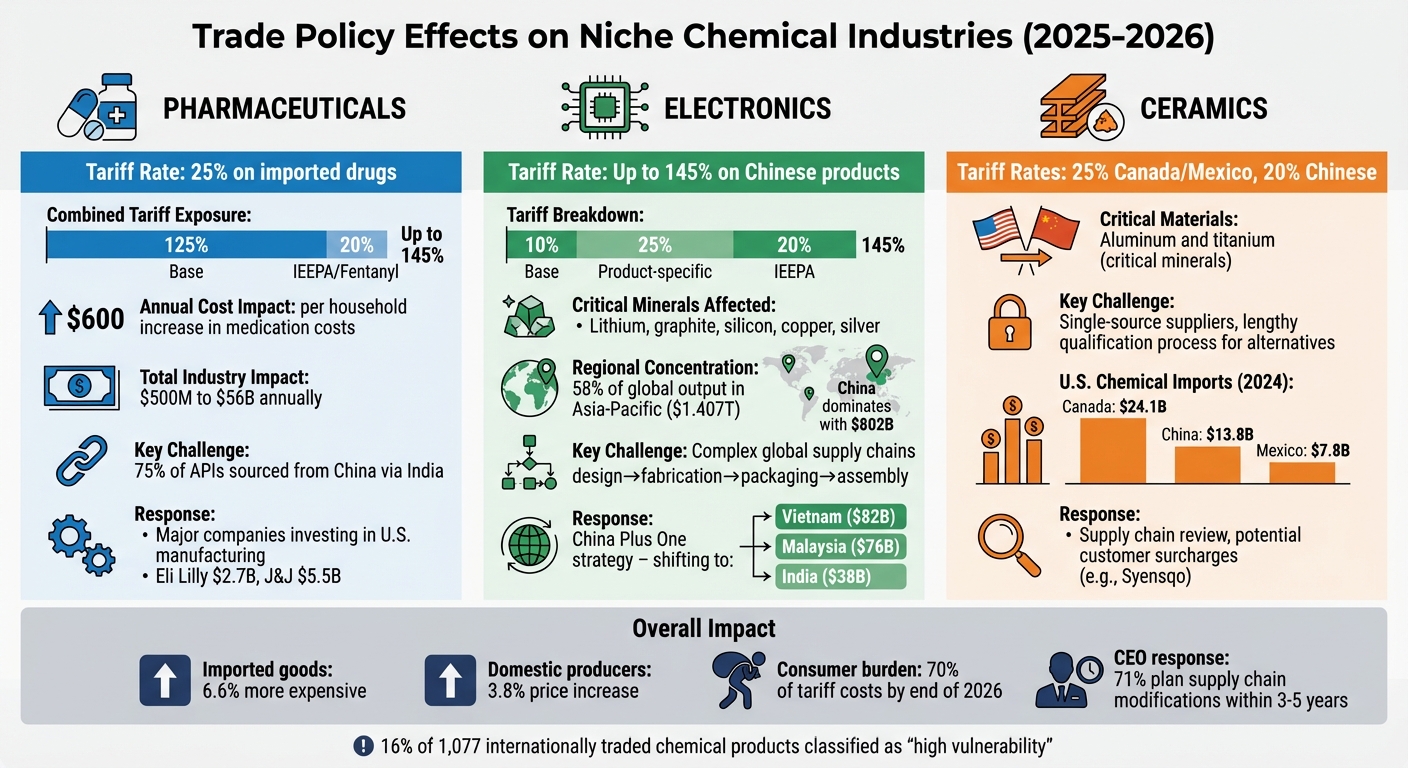

- Pharmaceuticals: Tariffs on intermediates and active ingredients may increase medication costs by $600 per household annually, with some producers exiting the market due to unsustainable costs.

- Electronics: Tariffs on critical minerals like lithium and silicon are driving up production costs, reducing competitiveness in global markets.

- Ceramics: Higher costs for raw materials like aluminum and titanium are delaying production while limiting supplier options.

Current Tariff Landscape:

- Pharmaceuticals: 25% tariff on imported drugs, including generic and biosimilar products.

- Electronics: Combined tariffs on critical minerals reaching up to 145%.

- Ceramics: 25% tariffs on imports from Canada and Mexico; 20% on Chinese goods.

With tariffs now covering specialty intermediates without exemptions, companies are rethinking supply chains. Strategies like "China Plus One" and shifting production to countries like Mexico, Vietnam, and India are gaining traction. Domestically, investments in U.S. manufacturing aim to reduce dependency on imports but come with higher labor costs.

Manufacturers are advised to diversify suppliers, monitor tier-2 and tier-3 risks, and consider tools like Foreign Trade Zones to manage costs. The evolving trade environment demands careful planning to navigate these challenges effectively. For ongoing updates on market shifts, stay informed through our industry newsletters.

2025-2026 U.S. Tariff Impact on Pharmaceutical, Electronics, and Ceramics Industries

Assessing The Impact Of Trump’s 25% Tariffs & Addl Penalty On India On OMCs & Chemical Sector

sbb-itb-aa4586a

How Tariffs Affect Specialty Chemicals and Intermediates

Tariffs have become a significant financial burden on specialty chemicals and intermediates, materials often sourced from single suppliers with no domestic alternatives. When these duties are imposed, manufacturers face tough decisions: absorb the additional costs, pass them on to customers, or overhaul their supply chains entirely.

Cost Changes from Tariffs

The financial strain caused by tariffs is both immediate and intense. For example, in March 2025, specialty chemical producer Syensqo announced a complete review of its supply chain strategy in response to new U.S. tariffs. This review included consideration of passing increased costs onto customers [1]. Across the industry, similar scenarios are playing out as companies struggle with shrinking profit margins.

Imported goods subject to tariffs have become 6.6% more expensive, while domestic producers have raised their prices by 3.8%. By the end of 2026, U.S. consumers were shouldering 70% of these tariff-related costs [5]. Even companies that source materials domestically are feeling the pinch, as higher prices ripple through the market.

For exporters, the situation is even more challenging. U.S. manufacturers that rely on imported chemical inputs face higher production costs, reducing their competitiveness in global markets [8]. They are caught in a difficult position – paying more for raw materials while competing against foreign manufacturers who don’t face the same cost pressures. This dynamic has strained supplier relationships and further complicated production strategies.

Supply Chain Disruptions

Tariffs not only drive up costs but also wreak havoc on supply chains. Research shows that tariffs on specialty chemical intermediates have led to the breakdown of long-standing U.S. buyer–foreign supplier relationships and a decrease in the formation of new ones [8]. Economists Kyle Handley, Fariha Kamal, and Ryan Monarch highlighted this trend:

"The decline in imports of tariffed goods was driven by discontinuations of U.S. buyer–foreign supplier relationships, reduced formation of new relationships, and exits by U.S. firms from import markets altogether." [8]

This disruption triggers production delays, especially for manufacturers dependent on intermediates without domestic substitutes. Without tariff exemptions, companies are left with two options: absorb the added costs or undertake costly and time-consuming supply chain overhauls [1]. Many firms adopt a "wait-and-see" approach, postponing major technological investments or production shifts due to the uncertainty surrounding trade policies [6].

The pharmaceutical industry is particularly vulnerable. Generic drug manufacturers, which often operate on razor-thin margins, are being forced to exit certain markets when production becomes unsustainable [4]. Switching to alternative suppliers – who may offer less reliability or higher costs – only adds to the instability of production schedules [7].

Disclaimer: This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

Effects on Pharmaceuticals, Electronics, and Ceramics

Tariff policies are creating significant challenges for industries that depend on specialized materials, with the pharmaceutical, electronics, and ceramics sectors being particularly affected. These sectors are grappling with rising costs and supply chain disruptions that threaten their operations and profitability.

Pharmaceuticals: Challenges in Sourcing Compendial-Grade Chemicals

The pharmaceutical industry is experiencing steep cost increases. Tariff measures are projected to escalate from $500 million to nearly $56 billion annually, leading to an average increase of $600 per year in household medication costs [11][3][2]. For generic drug manufacturers, who often operate on tight margins, these rising input costs could force them to stop producing low-margin but essential medications.

A major pain point lies in sourcing compendial-grade chemicals, which are primarily produced in China [1]. India, a key supplier of finished drugs to the U.S., imports about 33% of its active pharmaceutical ingredients (APIs) by volume, with 75% of these coming from China [12]. This dependence on Chinese imports creates a ripple effect: tariffs on Chinese goods impact not just direct U.S. imports but also medications manufactured in India.

Some Chinese imports now face combined tariffs as high as 145%, including a 125% base tariff and an additional 20% imposed under IEEPA and Fentanyl-related measures [11]. Eli Lilly CEO David Ricks explained:

"Drug companies like his would be forced to take on the full burden of tariffs rather than pass the costs to consumers because there are so many controls on the price of medicines" [2].

Robert Helminiak, Vice President of Legal and Government Relations at SOCMA, added:

"The executive order is explicit in that there are no exemptions" [1].

To mitigate future risks, major pharmaceutical companies – including Eli Lilly, Johnson & Johnson, Merck, Roche, and Novartis – announced significant investments in U.S.-based manufacturing facilities in early 2025, following the potential imposition of 25% tariffs on pharmaceuticals [2].

Electronics: Rising Costs for Critical Minerals

Electronics manufacturers face mounting challenges from tariffs, with rates on Chinese products reaching up to 145% when combining a 10% base tariff, 25% product-specific tariffs, and 20% IEEPA-related measures [11][3]. This is particularly problematic for a sector already heavily concentrated in the Asia-Pacific region, which accounts for 58% of global electronics output, valued at $1.407 trillion. China alone contributes $802 billion to this total, dominating electronics assembly as of 2023 [13].

Critical minerals like lithium, graphite, silicon, copper, and silver are essential for electronics production. The 2025 U.S. List of Critical Minerals added materials such as silicon, copper, silver, rhenium, and lead due to their economic importance and high supply chain risks [14]. These minerals are crucial for manufacturing semiconductors, batteries, and circuit boards.

The global nature of electronics production complicates matters further. For example, a semiconductor might be designed in the U.S., fabricated in Taiwan, packaged in Malaysia, and assembled in China. A disruption in any one region can halt the entire production process [13]. Tariff rates are determined by "substantial transformation" rules, adding administrative complexity to already strained supply chains [12].

To adapt, companies are diversifying their production locations under "China Plus One" strategies. Emerging hubs like Vietnam ($82 billion in output), Malaysia ($76 billion), and India ($38 billion) are becoming popular alternatives [13]. These shifts underline the changing dynamics of global electronics manufacturing.

Ceramics: Higher Raw Material Costs and Delays

The U.S. ceramics industry is grappling with rising costs for raw materials and production delays. Tariffs of 25% on goods from Canada and Mexico, along with 20% on Chinese goods, have forced manufacturers to reassess their supply chains for critical minerals like aluminum and titanium [1][15].

In March 2025, specialty chemical producer Syensqo announced plans to reevaluate its global supply chain strategy and suggested it might impose surcharges on customers to offset the financial impact of tariffs [1]. Ceramics manufacturers face additional risks when relying on single-source suppliers for critical materials. Both aluminum and titanium are classified as critical minerals due to their essential roles in production and vulnerability to supply disruptions [15].

Supply chain delays are further exacerbated by the time required to qualify new suppliers. Ceramic formulations often depend on specific particle sizes, purity levels, and chemical compositions. Switching suppliers can necessitate revalidating entire production processes, a task that can take months. Adding to the challenge, fewer than 20% of tariff exclusion requests were approved during prior trade disputes, and the 2025 policy has eliminated the exclusion process altogether [1].

In 2024, the U.S. imported $24.1 billion in chemicals from Canada, $13.8 billion from China, and $7.8 billion from Mexico [1]. These three countries are the largest U.S. trading partners for chemicals. Retaliatory tariffs, such as Canada’s 25% levy on $30 billion worth of U.S. goods in March 2025, have further compounded the issue [1]. Such measures highlight the interconnected challenges facing the ceramics industry in a volatile trade environment.

Supply Chain Diversification and Adaptation Methods

In response to tariff challenges, niche chemical industries are rethinking their supply chains. A survey of U.S. CEOs revealed that 71% plan to modify their supply chains within the next three to five years [18]. This shift marks a departure from the traditional "just in time" model, focusing instead on a "just in case" approach. This strategy prioritizes resilience, enabling companies to adapt and recover more effectively from trade disruptions [17].

Changes in Sourcing Regions

The "China Plus One" strategy has become a popular approach for companies seeking alternatives to Chinese sourcing. In 2023, Mexico overtook China as the top U.S. import partner for manufactured goods [18]. This trend, often referred to as the "Great Reallocation", involves shifting supply chains to countries like Vietnam and nearshoring options such as Mexico [16][19]. Southeast Asian nations, including Vietnam, Malaysia, Thailand, and Indonesia, are emerging as key hubs for specialty chemical intermediates [22][24].

India is also gaining recognition as a reliable partner for chemical manufacturing, offering seasoned expertise and reduced supply chain risks [21][22]. Brazil has become another attractive option, leveraging its abundant natural resources and growing manufacturing capabilities [24]. However, rising demand has pushed up import prices in both Vietnam and Mexico [16].

Domestically, U.S. sourcing is gaining traction due to its shorter lead times, reliable deliveries, and avoidance of international duties [23]. For example, Eli Lilly announced a $2.7 billion investment in four new U.S. plants to produce chemical ingredients, citing rising shipping costs and the need for a stable energy supply [23]. Similarly, Johnson & Johnson plans to invest $5.5 billion over four years to expand U.S. operations, including new facilities for chemical inputs, ensuring product reliability and reducing geopolitical risks [23].

As companies diversify their supply chains, ensuring supplier reliability remains a top priority.

Benefits of ISO-Certified Suppliers

ISO-certified suppliers play a crucial role in maintaining consistent product standards during supply chain transitions. These certifications help companies avoid quality issues and delays when onboarding new partners [18]. For complex chemical products, like compendial-grade chemicals for pharmaceuticals or high-purity materials for electronics, ISO certification ensures precision and compliance with regulatory standards [18]. It also simplifies the vetting process for secondary or alternative suppliers, helping businesses meet Customs and Border Protection (CBP) requirements and avoid risks tied to forced labor concerns or the Uyghur Forced Labor Prevention Act (UFLPA) [9].

Allan Chemical Corporation offers ISO-certified specialty chemicals for industries like pharmaceuticals, ceramics, and electronics. Their strong relationships with vetted manufacturers and just-in-time delivery capabilities help companies navigate supply chain challenges while maintaining strict compendial-grade standards (USP, FCC, ACS, NF) required in regulated sectors.

Sourcing Region Comparison

Understanding the trade-offs between sourcing regions is essential for managing tariff risks and operational reliability. Each region offers unique advantages and challenges. For instance, China remains a leader in specialty intermediates but faces high tariff exposure due to reciprocal tariffs, Section 301 duties, and additional surcharges [22]. Mexico benefits from nearshoring and USMCA agreements but is seeing rising import costs and potential policy shifts [16][18].

Southeast Asian countries, such as Vietnam, offer low labor costs but face higher tariffs – up to 46% – and longer lead times compared to Mexico [16][22]. Meanwhile, domestic U.S. sourcing eliminates tariff risks and ensures supply security but comes with higher labor costs and potential talent shortages [18].

| Region | Tariff Exposure | Primary Advantage | Key Risks |

|---|---|---|---|

| China | High tariff exposure [22] | Dominant producer of specialty intermediates | Geopolitical tensions; UFLPA compliance risks [9] |

| Mexico | 25% supplemental [18] | Proximity (nearshoring); USMCA benefits | Rising import prices; potential policy changes [16][18] |

| Vietnam | 46%+ [22] | Low labor costs | Higher prices; longer lead times [16] |

| U.S. Domestic | None | High quality; supply security; no tariff risk | Higher labor costs; talent shortages [18] |

Among 1,077 internationally traded chemical products (classified by HS code), 16% are considered "high vulnerability" due to limited domestic production and heavy reliance on Chinese imports [20]. This highlights the importance of mapping supply chain exposure down to tier 2 and tier 3 suppliers to identify potential risks and address tariff or detention concerns [9][18].

This content is for informational purposes only. Consult official regulations and qualified professionals before making sourcing or formulation decisions.

Conclusion: Managing Trade Policies in Niche Chemical Industries

Key Points for Procurement Leaders

Trade policies are reshaping how niche chemical industries secure raw materials and manage their supply chains. Utilizing 3PL for industrial chemicals can further streamline logistics and compliance. To navigate these changes, procurement leaders should focus on advanced planning and diversify their supplier base to minimize risks tied to tariff fluctuations. It’s also crucial to map tier-2 and tier-3 supplier exposure to anticipate potential risks like border delays or sudden duty increases [9][18].

Working with reliable suppliers, such as Allan Chemical Corporation, can help ensure consistent quality and on-time delivery of compendial-grade chemicals for industries like pharmaceuticals and electronics. These suppliers also assist in managing tariff challenges while meeting regulatory standards (USP, FCC, ACS, NF) [18]. Additionally, auditing contracts to include pricing flexibility and "change in law" clauses can allow businesses to share or pass on unexpected tariff costs rather than absorbing them entirely [9][18].

Future Trade Policy Changes and Chemical Supply Chains

Looking ahead, the trade landscape is expected to remain challenging, with potential new tariffs ranging from 10% to 25% on key trading partners and the possibility of 100% tariffs on BRICS nations [9][18]. Recent executive orders suggest stricter policies, with no exemptions for specialty chemicals sourced internationally, increasing tariff exposure for niche industries [1].

Companies should also prepare for retaliatory duties from trading partners, which could affect U.S. chemical exports like polyethylene [1]. To stay agile, consider leveraging Foreign Trade Zones (FTZs), bonded warehouses, and duty drawback programs to delay or reduce tariff payments on goods destined for re-export. Front-loading imports ahead of tariff implementations can also help secure short-term supply at lower costs [10][18].

This content is for informational purposes only. Always consult official regulations and qualified professionals when making sourcing or formulation decisions.

FAQs

What steps can niche chemical industries take to reduce the impact of U.S. tariffs on their supply chains?

Niche chemical industries can tackle the challenges posed by U.S. tariffs through strategies like reshoring production to the United States. By bringing manufacturing back home, companies can reduce their dependence on imported materials, sidestep tariff-related costs, and build a more resilient supply chain. This shift also allows for greater control over sourcing and can significantly cut down lead times.

Another smart move is diversifying suppliers. By sourcing materials from countries with lower or no tariffs, or by developing alternative materials to replace those subject to high taxes, companies can manage costs more effectively and reduce the risk of supply chain disruptions. Additionally, forming strategic partnerships and prioritizing innovation can boost operational efficiency, helping to counterbalance the rising costs of raw materials.

Allan Chemical Corporation plays a key role in supporting these initiatives by providing flexible sourcing options, just-in-time delivery, and a broad selection of specialty chemicals tailored for regulated industries. These efforts empower businesses to navigate changing trade policies while keeping their supply chains stable and reliable.

How are companies managing rising costs in specialty chemical intermediates?

Companies in specialized chemical sectors are finding creative ways to manage the rising costs of specialty chemical intermediates, a challenge largely driven by trade policies and tariffs. One common approach involves rethinking supply chains – evaluating raw materials and components to limit tariff exposure and cut expenses. Some businesses are also branching out by diversifying their suppliers, strengthening ties with domestic sources, or seeking international partners in regions less affected by trade restrictions to build stronger supply chain resilience.

On top of that, many companies are focusing on smarter inventory management and better use of working capital to handle supply chain disruptions and price shifts. This might mean fine-tuning inventory levels or adopting just-in-time delivery systems to stay agile. Companies like Allan Chemical Corporation play a critical role here, providing dependable sourcing and competitive pricing for technical-grade and compendial-grade chemicals. Their support helps businesses stay efficient and competitive, even in a challenging market environment.

How do current trade policies impact industries like pharmaceuticals, electronics, and ceramics?

Industries like pharmaceuticals, electronics, and ceramics are especially impacted by trade policies because they rely heavily on global supply chains for their raw materials and components. Tariffs and trade restrictions can create ripple effects, leading to increased costs, delays in supply chains, and even shortages.

Take the pharmaceutical industry as an example. Tariffs on ingredients and packaging materials can drive up production costs and heighten the risk of drug shortages, posing serious challenges. Similarly, the electronics and ceramics sectors, which depend on imported components and specialized materials, often face price increases and production delays when trade barriers arise. These industries are highly sensitive to shifts in global trade policies, where even minor disruptions can have a major effect on their operations and ability to stay competitive.

Comments are closed